Hello, if you have any need, please feel free to consult us, this is my wechat: wx91due

Advanced Econometrics I

EMET4314/8014

Semester 1, 2025

Assignment 9

(due: Tuesday week 10, 11:00am)

Exercises

Provide transparent derivations. Justify steps that are not obvious. Use self sufficient proofs. Make reasonable assumptions where necessary.

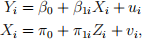

In the lecture we learned about the potential outcomes framework. Translated into a regression model, it can be represented by

where

This looks like a two stage regression in which the slope coefficients are individual-specific. You have iid sample data (Xi , Yi , Zi) and compute  . From the week 5 lecture you know

. From the week 5 lecture you know

where sZY denotes the sample covariance and σZY denotes the population covariance of Zi and Yi (and likewise for the objects in the denominator).

The goal here is to present σZY and σZX in terms of moments of π1i and β1i . In your deriva-tions, please assume random assignment of Zi so that

(i) Prove that

(Note: π1i was defined in the lecture)

(ii) Prove that

(Note: β1i was defined in the lecture)

Putting things together: = E(β1iπ1i)/E(π1i) + op(1). We called the probability limit the local average treatment effect (LATE).