Hello, if you have any need, please feel free to consult us, this is my wechat: wx91due

DEPARTMENT OF STATISTICS AND ACTUARIAL SCIENCE

STAT3909 LIFE CONTINGENCIES II

May 11, 2024

Time: 6:30 p.m. 一 9:30 p.m.

S&AS: STAT3909 Life Contingencies II

1. You are given the following information about a fully discrete 10-year endowment insurance policy on (55):

• The sum insured of 100,000 is payable at the end of the year of death, or upon survival to age 65.

• A premium of 8,500 is payable at the beginning of each year.

• The net premium, as determined by the equivalence principle, is 6,700.

• Expenses on the policy are as follows:

一 Initial expense: 10% of the first premium plus 2,000;

一 Renewal expense: 5% of subsequent premiums plus 600;

一 Termination expense: x% of the sum insured.

• Initial and renewal expenses are to be paid at the beginning of each year, while the termination expense is to be paid at the same time as the benefit payment.

• i = 0.08.

The expense policy value at time t = 9 years is 2,465. Calculate the value of x. [Total: 5 marks]

2. (a) Explain clearly the meaning of the actuarial symbol  . [3 marks]

. [3 marks]

(b) Assume that (x) and (y) have independent future lifetimes. Using the integral calculation formulas for actuarial present values, simplify  + . [4 marks] [Total: 7 marks]

+ . [4 marks] [Total: 7 marks]

3. In a two-decrement model, it is known that:

•  = 0. 15, t ∈ [0, 1] .

= 0. 15, t ∈ [0, 1] .

•  = 0.2.

= 0.2.

• Decrement 2 is uniformly distributed within each year of age in the associated single decrement model.

(a) Show that

for t ∈ [0, 1] . [3 marks]

(b) Calculate  . [5 marks]

. [5 marks]

[Total: 8 marks]

4. The following information on a whole life insurance policy issued to (50) is available:

• A benefit of 100,000 is paid at the end of the year of death.

• The death benefit is doubled if the policyholder dies while performing his duties at work.

• The insurer assumes a two-decrement model, with decrement 1 being “non- occupational death” and decrement 2 being “occupational death”.

• The policyholder pays a premium of 2,000 at the beginning of each year.

• No expense is assumed.

• i = 0.05.

•  = 0. 11,

= 0. 11,  = 0.24 at i = 0.05.

= 0.24 at i = 0.05.

•  = 0.01,

= 0.01,  = 0.014.

= 0.014.

• Decrements are assumed to be uniformly distributed in the multiple decrement table.

(a) Show that  to the nearest 0.5. You should calculate this value to the nearest 0.01 to ensure su!cient accuracy in subsequent calculations. [2 marks]

to the nearest 0.5. You should calculate this value to the nearest 0.01 to ensure su!cient accuracy in subsequent calculations. [2 marks]

(b) Calculate the exact value of 9.5v, the policy value at time t = 9.5 years, by first obtaining the value of 10v. [7 marks]

[Total: 9 marks]

5. Two lives, (x) and (y), are such that their lifetime random variables Tx and Ty are independent and identically distributed. Each lifetime follows the continuous uniform distribution between 0 and 10.

(a) Show that the survival function of Txy is given by

when 0 ≤ t ≤ 10. Hence, calculate  and Var(Txy) . [8 marks]

and Var(Txy) . [8 marks]

(b) Calculate

[Hint: The mean and variance of a Uniform(a, b) random variable are (a + b)/2 and (b ↓ a)2 /12, respectively.] [6 marks]

(c) Does your answer in part (b) depend on the upper bound of the uniform distribu- tion, assumed to be 10 in this question? Explain your answer. [3 marks]

[Total: 17 marks]

6. You are given the following information on a fully discrete 5-year term insurance policy issued to (60):

• A benefit of 10,000 is paid at the end of the year of death.

• A level premium is paid at the beginning of each policy year.

• Expenses are as follows:

一 Pre-contract expense: 200;

一 Recurring expense: 75 at the beginning of each policy year including the first;

一 Settlement expense: 5% of the death benefit, incurred at the same time as the death benefit payment.

• q62 = 0. 12.

• i = 0.06.

In a profit test conducted by the insurance company, the insurer sets the following reserves at the end of each policy year:

(a) The insurer finds that the profits for the third and fourth policy years are 143.3 and 13.3 for each in-force policy at the beginning of the respective years. Calculate the value of q63 used in the profit test. [4 marks]

In the following two parts, assume that the insurer conducts a profit test based on another scenario with the following quantities:

• Annual premium: 1,220;

• Survival and mortality rates: 2p60 = 0.8648, q63 = 0. 16, q64 = 0. 18. Other assumptions and the end-of-year reserves remain unchanged.

(b) It is known that the first four elements of the profit signature are

(σ0, σ1, σ2, σ3) = (↓200, 113.7, 157.64, 160.59) .

Show that the policy has an internal rate of return between 20% and 25%. [6 marks]

(c) Calculate the zeroized reserves at the end of the third and fourth policy years. [4 marks]

[Total: 14 marks]

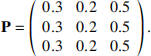

7. A discrete-time Markov chain with three states is used to model the status of (x) . The

states are labelled as 0, 1, 2, and the transition probability matrix is as follows:

Transitions occur at the end of each year, before the determination of benefits. A whole life insurance policy on (x), who is currently in state 0, has the following terms:

• A benefit of 10,000 is paid at the end of each year that (x) is in state 1.

• The policyholder pays a premium of G at the beginning of each year that (x) is in state 0.

• Expenses are 10% of each premium.

Let i = 0.08.

(a) Calculate the value of G based on the equivalence principle.

[Hint: Calculate P2 . What do you observe?] [5 marks]

(b) Without doing any calculations, explain whether:

i. 1v(1) is larger than, smaller than, or equal to 1v(2);

ii. 1v(1) is larger than, smaller than, or equal to 2v(1) . [5 marks]

[Total: 10 marks]

8. A continuous reversionary annuity of rate 1 per annum issued to (x) and (y) has the following terms:

• The benefit payment starts after the death of (x) or after 10 years, whichever is later, if (y) is still surviving at that time.

• After the commencement of benefit payment, it will continue until the death of (y) .

• No benefit will be paid in all other circumstances.

(a) Show that the actuarial present value of this reversionary annuity is equal to

Explain this result intuitively. [5 marks]

(b) Suppose the status of the lives (x) and (y) are modelled using a multiple state model with four states being: (0) — both are alive; (1) — only (x) is alive; (2) — only (y) is alive; (3) — both are dead. For a policy with benefit being the continuous reversionary annuity stated above and premium payable as a lump sum at the inception of the policy, express 5v(i) in terms of single-life and reversionary annuity symbols for i = 0, 1, 2, 3. [4 marks]

[Total: 9 marks]

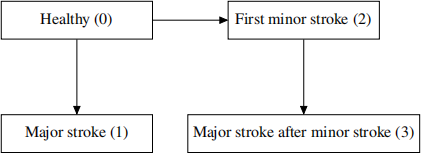

9. Stroke is a potentially life-threatening medical condition caused by a lack of blood supply to the brain cells. A stroke can be classified as “minor” or “major” . A 20-year insurance policy issued to (x), who is currently healthy, provides the following benefits:

• A sum of 500,000 is paid immediately upon the diagnosis of a major stroke that is not preceded by any minor strokes (“Benefit 1”).

• A sum of B is paid immediately upon the diagnosis of the first minor stroke (“Benefit 2”).

• A sum of 200,000 is paid immediately upon the diagnosis of a major stroke that is preceded by one or more minor strokes (“Benefit 3”).

The policy expires upon the payment of a major stroke benefit, whether or not it is preceded by minor strokes. The insurer uses the following continuous-time multiple state model to describe the health status of (x):

The forces of transition are:  = 0.03,

= 0.03,  = 0.08, and

= 0.08, and  = 0. 14 for all t ≥ 0 (in years). Let δ = 0.05.

= 0. 14 for all t ≥ 0 (in years). Let δ = 0.05.

(a) Express  in terms of t (for t ≥ 0), and show that the probability that (x) will suffer a minor stroke but not a major stroke in the next 20 years is 0.13 to the nearest 0.01. [5 marks]

in terms of t (for t ≥ 0), and show that the probability that (x) will suffer a minor stroke but not a major stroke in the next 20 years is 0.13 to the nearest 0.01. [5 marks]

(b) Using Euler’s method on the Kolmogorov forward equations with step size h = 0.25, approximate the probability that (x) will su"er a minor stroke but not a major stroke in the next 20.25 years. [3 marks]

(c) The insurer wants to set the value of B, the benefit for the first minor stroke, such that the actuarial present value of Benefit 1 is equal to the sum of the actuarial present values of Benefits 2 and 3. Calculate the value of B. [7 marks]

(d) Suppose that (x) has su"ered a minor stroke but not a major stroke by time t = 10 years. Let L be the future loss random variable at that time. No further premiums are to be paid. Calculate the probability that L is larger than 150,000. [4 marks]

(e) Describe one deficiency of the multiple state model assumed by the insurer. [2 marks]

[Total: 21 marks]