Hello, if you have any need, please feel free to consult us, this is my wechat: wx91due

Financial Statement Investigation

Accounting for International & Public Affairs

Mid-Term Examination

Course U6200

October 25, 2018

Bedding Markdowns, Inc.

On Saturday, December 31, 2016, Sheila and Keith Minter signed the final legal documents so they could begin operation on January 1, 2017 of their new business venture, Bedding Markdowns, Inc. in Omaha, Nebraska. To provide initial financing for the business on December 31, 2016, Sheila and Keith invested $300 thousand of their savings for 60% of the common stock (owners’ capital) of Bedding Markdowns. In addition, on December 31, 2016, Sheila and Keith’s parents invested $200 thousand for 40% of the common stock (owners’ capital) of Bedding Markdowns.

Furthermore, the following additional transactions for Bedding Markdowns took place prior to Bedding Markdowns beginning operations on January 1, 2017:

1. On December 31, 2016, Sheila & Keith’s uncle, Ken Johnson, paid Bedding Markdowns $100 thousand for mattresses for a new hotel he owned in Omaha. The new hotel would not be ready to receive the mattresses until it was completed in early 2017.

2. On December 31, 2016, Bedding Markdowns took delivery of $300 thousand worth of office and showroom floor furnishings and fixtures. All of the furnishings and fixtures were paid for as of December 31, 2016.

3. On December 31, 2016, $400 thousand of an initial mattress inventory was purchased on ac-count and would be paid for at the end of February 2017.

4. On December 31, 2016, Bedding Markdowns prepaid its fire and casualty insurance policy premium of $60 thousand covering the 12 months ended December 31, 2017.

All of these initial transactions are reflected in the following Balance Sheet for Bedding Mark-downs as of December 31, 2016, prior to the Company beginning operations.

BEDDING MARKDOWNS

Statement of Financial Position (Balance Sheet) as of December 31, 2016

(all dollar amounts in thousands)

Background

The Minters had lived in Omaha all of their lives. For the past few years, both Sheila and Keith worked in the home furnishings department of The Emporium department store in downtown Oma-ha. Sheila was a sales person in the furniture and rugs department and Keith was a sales person in the bedding department. During their time at The Emporium, the Minters developed a number of strong business relationships with the sales people from the various home furnishings manufacturers that sold to The Emporium. On numerous occasions, the manufacturing sales representatives would tell the Minters, “You are so good at selling, you should go into business for yourselves”. Over time, Sheila and Keith began to consider the possibility of starting their own business.

At a family gathering during the summer of 2016, the Minters discussed their entrepreneurial ideas with Ken Johnson, one of Sheila’s uncles. Mr. Johnson had recently retired as a senior marketing executive from Beauty Sleep, Inc. (“BSI”), the best-selling manufacturer of mattresses in the United States. He explained to the Minters how manufacturers like BSI would offer sub-stantial price reductions on its brand-name mattresses to discount retailers due to overproduction of a certain line of mattresses or because they were phasing out a line of mattresses.

In September 2016, the Minters met again with Ken Johnson. He had made contact with sen-ior marketing executives that he knew at a number of brand name mattress manufacturers. All of the executives had agreed to allow the Minters to become purchasers of their discounted mattress lines as they became available. The Minters decided to move forward with opening the first Bed-ding Markdowns store on January 1, 2017. The Minters would be actively involved with the day to day operations of the store, for which they would receive a salary.

As was mentioned earlier, at the end of December 2016 the Minters finalized the initial fi-nancing and investment for Bedding Markdowns as well as the purchase, on account, of the ini-tial mattress inventory (see Statement of Financial Position (Balance Sheet) on page 2).

On Saturday, January 1, 2017, Bedding Markdowns began operations in a small, stand alone building to be used as the Bedding Markdowns retail store. The building was located in a “strip mall” on the main road leading into downtown Omaha. Throughout calendar-year 2017, the Mint-ers worked full time operating Bedding Markdowns. In addition, they hired a number of full-time and part-time employees for selling, cleaning and miscellaneous jobs around the store.

It was now 6:30 P.M. on Sunday, December 31, 2017. For both tax purposes and financial reporting (“book”) purposes, the Minters had chosen December 31st as their fiscal year end for Bedding Markdowns. For tax purposes, they wanted to file their fiscal 2017 tax return for Bed-ding Markdowns as soon as possible. On December 15, 2017, they had made an estimated tax payment to the Internal Revenue Service for the 12 months ended December 31, 2017. The Mint-ers were anxious to learn if they might be entitled to a tax refund or if they would have to make any additional tax payments. In addition, they were hoping to use their “book” financial state-ments to assist them in determining whether or not opening a second Bedding Markdowns store in 2018 would be possible.

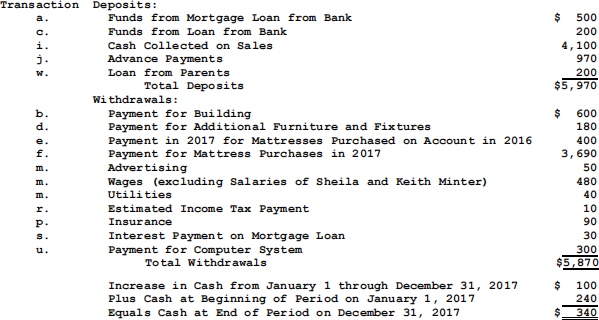

The Minters put their records together and met with their friend Debra Horwath, a local C.P.A. and tax accountant. The only records that the Minters kept for their business were a checkbook register, which included detailed explanations of all checks drawn, a file of all invoices received, and a list of sales made on account from credit card sales and commercial sales. A summary of Bedding Markdowns’ cash deposits and withdrawals for 2017 is provided on the next page.

Summary of Cash Deposits and Withdrawals, January 1, 2017 – December 31, 2017

(all dollar amounts in thousands)

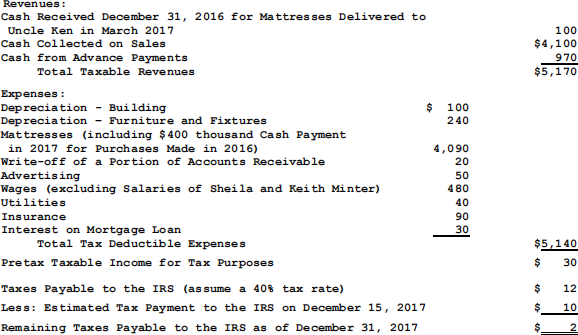

Ms. Horwath took the Minters’ records to her office where she completed the following tax return for Bedding Markdowns for the 12 months from January 1, 2017 through December 31, 2017.

Tax Return for the Twelve Months from January 1, 2017 through December 31, 2017

(prepared on a cash basis except for depreciation and write-off of accounts receivable)

(all dollar amounts in thousands)

While the Minters were happy to learn that Bedding Markdowns had made a profit for tax purposes, they were a little perplexed by the tax results. In a meeting with Debra, Keith said, “The tax return results are surprising. I thought the Company did better than the return shows.” Debra Horwath responded, “Keith, you have to understand that the tax return is not the same as an income statement based on accrual accounting. There are some adjustments that I will need to make to transform your tax return into a set of financial statements that are based on the accrual accounting method. I don’t know what the results will be but I think the accrual method is likely to give you a better picture of Bedding Markdowns’ operation over the past 12 months” (from January 1, 2017 through December 31, 2017).

Debra concluded the meeting by telling the Minters that she would take the information she had received from them and prepare a complete set of financial statements using the accrual meth-od of accounting. They agreed to meet on Wednesday, January 3, 2018 to discuss Debra’s results.

In beginning her preparation of the accrual accounting based financial statements for Bedding Markdowns for the 12 months ended December 31, 2017, the first thing Debra did was to prepare the opening balance sheet as of December 31, 2016 to reflect the initial transactions that Sheila and Keith had entered into with respect to Bedding Markdowns prior to the start of operations in January 2017 (see Statement of Financial Position (Balance Sheet) on page 2).

Next, Debra recorded (“bookkept”) the transactions that Bedding Markdowns had entered in-to since it opened for business on January 1, 2017. She began recording Bedding Markdowns’ transactions from the cash deposits and withdrawals record (see page four) for the Company from January 1, 2017 through December 31, 2017. Debra went through each of the cash transactions, making accrual accounting adjustments that she deemed necessary along the way, using the addi-tional information from the following transactions (all dollar amounts in thousands).

a. On January 1, 2017, the Company received $500 from Omaha Trust & Savings Bank in the form of a 10-year mortgage loan at an annual interest rate of 6%. Terms of the loan called for an interest only payment in the first year on December 31, 2017 (see transaction q. on page seven for further details regarding the repayment of interest and principal on the mort-gage loan).

b. On January 1, 2017, Bedding Markdowns paid $600 for the retail store building from which it would conduct its operations. Expected useful life of the building is 30 years (see transaction s).

c. On January 1, 2017, Bedding Markdowns received a $200 unsecured one-year loan (note payable) from Omaha Trust & Savings Bank due on January 1, 2018 at an annual interest rate of 10% (see transaction r on page seven for further details regarding the repayment of interest and principal on the note payable).

d. Also, on January 1, 2017, the Company purchased $180 of furniture and fixtures, which was in addition to the $300 it acquired on December 31, 2016 (see December 31, 2016 balance sheet). Expected useful life of the furnishings and fixtures is 6 years (see transac-tion s).

e. On February 28, 2017, Bedding Markdowns paid the $400 in accounts payable for its ini-tial mattress inventory which had been purchased and received on December 31, 2016.

f. Additional mattresses, bed frames, and headboards (collectively called “mattresses”) total-ing $4,000 were purchased on account throughout 2017. During the year, Bedding Mark-downs paid $3,690 for mattresses purchased on account in 2017. As a result, on December 31, 2017, the Company still owed mattress suppliers $310. It did not owe suppliers for any other items on December 31, 2017.

g. According to the Company’s records, on December 31, 2017, Bedding Markdowns still had in inventory $370 worth of mattresses.

h. In March 2017, Bedding Markdowns shipped the $100 mattresses Uncle Ken had ordered on account in December 2016 to Uncle Ken’s newly completed hotel.

i. In-store sales of Bedding Markdowns’ products were for cash or credit, with the vast ma-jority sold on credit by means of the Company accepting third-party credit cards. In addi-tion, the Company had quickly developed a credit relationship with a number of small commercial customers in the Omaha area. Sales made to these institutions involved a cash down payment and the remainder on credit, payable to Bedding Markdowns within 45 days of having been provided mattresses.

Through December 31, 2017, the Company received $4,100 in cash from customers through collections from credit card companies for sales made on account, cash payments for sales made to commercial accounts, and direct cash sales.

j. In addition to the $4,100 cash collected for sales through December 31, 2017, the Compa-ny received $970 in down payments for mattresses that will be provided to commercial customers in the first quarter of 2018.

k. On December 31, 2017, the credit card companies still owed Bedding Markdowns $570 for sales of mattresses made during December, 2017. The Company expected to collect all of the $570 owed from the credit card companies by the end of January, 2018.

l. Also on December 31, 2017, commercial accounts still owed Bedding Markdowns $400 for mattresses purchased from the Company during 2017. All of the commercial accounts were current except for one motel which still owed $40 (included in the $400 still owed to Bedding Markdowns) for mattresses it purchased from Bedding Markdowns at the begin-ning of June 2017. Unfortunately, the motel had closed at the end of August 2017 and filed for bankruptcy.

In December 2017, the bankruptcy court informed Bedding Markdowns that it could ex-pect to receive “somewhere between 0 cents and 50 cents on the dollar” for the $40 that it was owed. The court also noted that Bedding Markdowns would not receive any more than $20 of the $40 it was owed by the bankrupt motel. As a result, for the year ended December 31, 2017, Keith Minter decided to make an allowance for $20 of the $40 it was owed and to immediately “write-off” the remaining $20.

m. Advertising expenses of $50, wages of $480 (excluding the salaries of the Minters), and utilities of $40 had all been paid as of December 31, 2017. There were no outstanding ad-vertising, wages or utilities expenses.

n. The Minters earned a salary $135 apiece for the work they performed at the Company from January 1, 2017 through December 31, 2017. However, in order to bolster Bedding Mark-downs end of year cash position, the Minters decided to postpone receiving the $270 in sala-ries they earned in 2017 until 2018. They still had $300 in personal savings which they could “live off of” before being paid by Bedding Markdowns.

o. On December 15, 2017, the Company made an estimated income tax payment of $10 for Bedding Markdowns for the 12 month tax period from January 1, 2017 through Decem-ber 31, 2017.

p. During 2017, the Company’s insurance company raised its annual premium for 2018 cov-erage from $60 to $90. On December 31, 2017, Bedding Markdowns paid the $90 annual premium for fire and casualty insurance covering the 12 months ended December 31, 2018.

q. The annual interest of $30 on the mortgage loan was paid on its due date of December 31, 2017. Beginning on December 31, 2018, the principal and interest on the mortgage loan would be paid back in annual payments for the next 9 years

r. The principal of $200 and the annual interest of $20 on the note payable are both due on January 1, 2018. As of December 31, 2017 no principal or interest on the note payable had been paid.

s. Debra Horwath determined that for financial reporting (“book”) purposes, annual straight-line depreciation of $20 for the Company’s building over a 30-year useful life and $80 for the furnishings and fixtures over a 6-year useful life is appropriate.

She also noted that, for tax purposes, the building and the furnishings and fixtures would be depreciated on an accelerated basis for tax purposes in 2017 (see Tax Return on page 4 of the case).

t. On December 31, 2017, Bedding Markdowns purchased a new computer system for $300 which is expected to have a useful life of 6 years. Over the next 6 years, the new computer system was expected to reduce Bedding Markdowns operating expense by $50 per year.

u. On December 31, 2017, Sheila and Keith Minter, from their personal savings, purchased their parents 40% interest in the common stock of Bedding Markdowns for $200.

v. On December 31, 2017 Sheila and Keith’s parents lent Bedding Markdowns $200 in the form of a one year loan due on December 31, 2018 paying annual interest of $20.

Once she had completed bookkeeping all of these transactions, Debra began to piece together the information she needed to prepare: (a) an income statement for the twelve months beginning January 1, 2017 and ending December 31, 2017; (b) a balance sheet as of December 31, 2017; (c) a direct method and (d) an indirect method cash flow statement for the twelve months begin-ning January 1, 2017 and ending on December 31, 2017.

Questions:

1. Using the attached T-accounts (or any other method you prefer) and accrual accounting, as best you can record (“bookkeep”) the transactions for Bedding Markdowns from the period January 1, 2017 through December 31, 2017 (record all dollar amounts in thousands)..

2. Based on you answer to Question 1, for financial reporting purposes (not tax purposes) pre-pare, “in good form” (i.e. proper headings for the reports, distinguish such items as current assets and current liabilities; in the income statement, operating earnings = earnings before interest and taxes; specify all dollar amounts in thousands):

a. An income statement for the 12-month period from January 1, 2017 through December 31, 2017. Assume an income tax rate of 40% is appropriate for Bedding Markdowns.

b. A statement of financial position (i.e. balance sheet) as of December 31, 2017; and,

c. A statement of cash flows using the Direct Method for Bedding Markdowns for the 12-month period from January 1, 2017 through December 31, 2017; and,

d. A statement of cash flows using the Indirect Method for Bedding Markdowns for the 12-month period from January 1, 2017 through December 31, 2017.

As long as you show the investing and financing sections of the cash flow statement using the Direct Method approach, you do not need to show them again for the Indirect Method approach since they will be the same. For the Indirect Method cash flow statement, you do need to show the operating activities section.

3. Overall, do you think Bedding Markdowns had a “good” year or a “bad” year from January 1, 2017 through December 31, 2017? What criteria did you use to gauge Bedding Markdowns’ performance? As equity investors in Bedding Markdowns, should Sheila and Keith’s parents be satisfied? Why or why not?

4. Should the Minters be concerned about the Company’s cash position at December 31, 2017 with respect to operating their business in 2018? With respect to opening a second Bedding Markdowns store? Why or why not?

5. Two of the main requirements that the bank required to be met were: (1) the Company have earnings before interest and taxes of at least 2 times the Company’s interest expense; and (2) the Company maintain an end-of-the-year total (both current and long-term) “interest-bearing” debt to end-of-the-year owner’s equity ratio of no more than 1.75 to 1.

As of December 31, 2017, is Bedding Markdowns meeting the two requirements on its bank loan? Based on the information available to you in early January 2018, if you were the banker who lent Bedding Markdowns the $200 for general corporate purposes on January 1, 2017, would you be inclined to renew the $200 loan on January 1, 2018? On the same terms? Why or why not?

6. What are three individual differences between “book” and tax accounting for Bedding Mark-downs in 2017? Specify if the individual differences initiate a deferred tax liability or a de-ferred tax asset.