Hello, if you have any need, please feel free to consult us, this is my wechat: wx91due

MATH375: Tutorial 1

Tutorial 1

1. Let (Ω, F) = ([0, 1], B[0, 1]),and let

be two random variables.Let  be a probability measure on (Ω, F) defined as

be a probability measure on (Ω, F) defined as

Find µX [a, b] and µY [a, b].

2. Let f (x) denote the standard normal density function, which is defined as:

Also let N(x) denote the standard normal cumulative distribution function, which is defined as:

Let (Ω, F, P) be a probability space on which a standard uniform random variable Y is defined. Show that the random variable

is standard normal.

3. Let X be a random variable defined on (Ω, F, P) with exponential cumulative distribution function

where λ is a positive constant. Let  be another positive constant, and define

be another positive constant, and define

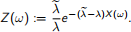

Define  as:

as:

(i) Show that (Ω) = 1,

(ii) Derive {X ≤ x}, −∞ < x < ∞, i.e. the cumulative distribution function of X under .

(iii) Derive  [X] and

[X] and  , i.e. the expected value and the variance of X under .

, i.e. the expected value and the variance of X under .