Hello, if you have any need, please feel free to consult us, this is my wechat: wx91due

1. Introduction to Time Series

ECO374H1

Department of Economics

Summer 2025

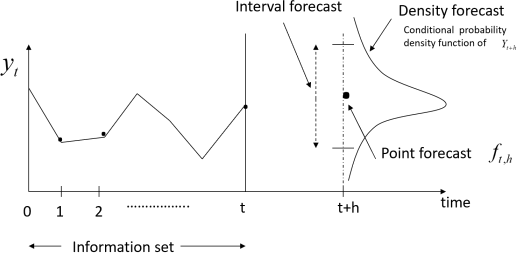

Forecaster's Objective

For illustration, see the code file 1. ACF and PACF (section 1)

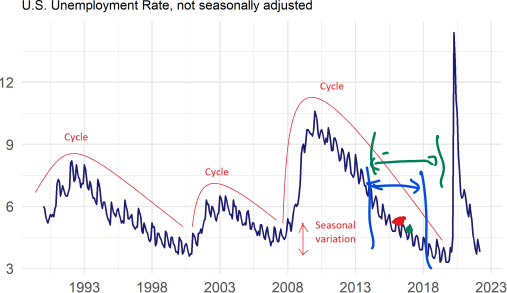

Features of Time Series

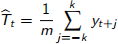

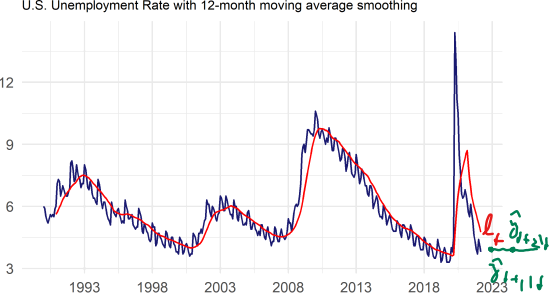

Moving Average Smoothing

Moving Average Smoothing (MAS) of order m:

where m = 2k + 1

Note that each data point has the same weight m/1

MAS is typically used for "seasonal adjustment" of data, i.e. filtering out seasonal variation to estimate the trend-cycle component

Simple Exponential Smoothing

Simple Exponential Smoothing (SES) assigns the most recent observation the most weight, and the most distant (in time) observation the least weight

Denote by  the trend-cycle component of {yt} at time t

the trend-cycle component of {yt} at time t

At time t we observe yt and can update our estimate of and predict yt+1:

=

=  yt + (1 - )-1

yt + (1 - )-1

yt+1|t =

assuming we know - 1

We can estimate e0 using an MAS of e.g. the first 10% of the data and then obtain subsequent recursively from the Smoothing equation

α is a smoothing constant such that 0 < α < 1

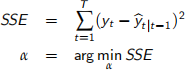

Smoothing Parameter in SES

For a data set  the optimal level of α can be determined by minimizing the sum of squared "in-sample" errors of one-period-ahead forecasts

the optimal level of α can be determined by minimizing the sum of squared "in-sample" errors of one-period-ahead forecasts

The minimization is performed numerically

SES Forecasts

SES has a "áat" forecast function

SES forecasts have limited use beyond very short time horizon forecasts (similarly for MA smoothing)

Nonetheless, SES weight distribution provides the backbone of many dynamic forecasting models that we will cover