Hello, if you have any need, please feel free to consult us, this is my wechat: wx91due

ECON0060: Problem Set 2

Due date: Monday, January 22 before your tutorial. Please attach a copy of the “Economics Department MSc Coursework Feedback Form” to your solution, and fill part I of the form.

Question 1

Consider the system of two simultaneous equations

yi1 = yi2α1 + xiβ1 + ui1,

yi2 = yi1α2 + wiβ2 + ui2.

where yi1 and yi2 are endogenous variables, and xi and wi are two exogenous regressors. There are four scalar structural parameters α1, α2, β1 and β2. The reduced form equations read

yi1 = xiπ11 + wiπ21 + εi1,

yi2 = xiπ12 + wiπ22 + εi2.

where π11, π12, π21, and π22 are the reduced form parameters.

(a) Assume that α1α2 ≠ 1. Find expressions for the reduced form parameters in terms of the structural parameters.

(b) Assume that π11 ≠ 0 and π22 ≠ 0. Show that all structural parameters are identi-fied. Find expressions for the structural parameters in terms of the reduced form parameters.

(c) Consider estimation of α1 and β1 by applying 2SLS to the first structural equation, using wi as an instrument for yi2. Why is the condition π22 ≠ 0 important for this 2SLS estimation? Can the parameters α1 and β1 be consistently estimated when π22 = 0?

Question 2

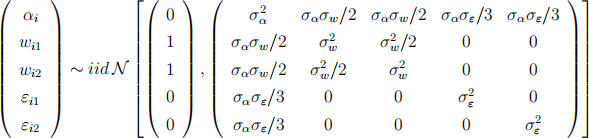

Consider the following panel data model with one regressor wit and two time periods

yit = β1 + witβ2 + αi + εit, i = 1, . . . , n, t = 1, 2.

We assume that

(a) Does this model satisfy the random effects assumptions? Is the random effects OLS estimator that regresses yit on a constant and wit consistent for β1 and β2?

(b) We now want to estimate the model using a fixed effect assumption on αi . Can we estimate β1 consistently? Can we estimate β2 consistently?

(c)

The within group and first difference OLS estimator for β2 are given by

Show that  .

.

(d) Write down the limiting distribution of  (you can use the theorem in the lecture slides). Find an expression for the asymptotic variance of

(you can use the theorem in the lecture slides). Find an expression for the asymptotic variance of  in terms of

in terms of  and

and  .

.

(e) We have the consistent estimator  and according to the above assumption we know that E(αi) = 0 and E(εit) = 0. Use these information to provide a consistent estimator for β1. Is this estimator consistent under a fixed effect assumption on αi?

and according to the above assumption we know that E(αi) = 0 and E(εit) = 0. Use these information to provide a consistent estimator for β1. Is this estimator consistent under a fixed effect assumption on αi?