Hello, if you have any need, please feel free to consult us, this is my wechat: wx91due

MATH39512 Survival Analysis for Actuarial Science: example sheet 1

*=easy, **=intermediate, ***=difficult

* Exercise 1.1

For a study rats were injected with a tumor-inducing substance called DMBA and the event of interest is the onset of a tumor. The observation period started at 1 November last year and lasted for 40 days. Unless mentioned otherwise each rat was given DMBA at 1 November. Consider the following five rats:

A: A rat who developed a tumor 28 days after receiving DMBA.

B: A rat who survived the study without having any tumors.

C: A rat who started being observed and got DMBA injected on 15 November and devel-oped a tumor 20 days later.

D: A rat who died (without tumor present and death was unrelated to the occurrence of cancer) at day 37 after receiving DMBA.

E: A rat who got DMBA injected 12 days before the start of the study/observation period and who survived the study without having any tumors.

(a) Assume the time scale is the time elapsed since DMBA was injected. Which of the above rats had censored survival times and which ones had truncated survival times?

(b) Same question as in (a) but now assume the time scale is the time elapsed since the start of the observation period (i.e. 1 November).

(c) Which of the two time scales is the most appropriate one for studying the effect of DMBA on the development of a tumor?

** Exercise 1.2

A machine consists of two components A and B. The producer wants to estimate the failure time due to the breakdown of component A of these type of machines. Therefore a number of machines will be observed. If one of these machines break down due to the failure of component B instead of A, then its resulting failure time will be considered a censored value. Describe a scenario in which this form of censoring is independent and one in which it is not independent. (Hint: the hypothetical situation where there is no censoring (of this form) corresponds to the situation where a failure of component B does not result in the failure of the machine.)

** Exercise 1.3

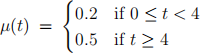

Suppose the following Cox proportional hazards model describes the mortality of a group of life-assurance policyholders:

µi(t) = µ0(t) exp (βx(xi − 30) + βyyi + βzzi),

where time t is time in years with t = 0 corresponding to the time of entry (i.e. the time when the life-assurance policy starts for a particular policyholder) and

• µi(t) denotes the hazard function for life i at time t,

• µ0(t) is the baseline hazard function at time t,

• xi denotes the age at entry (t = 0) of life i,

• yi = 1 if life i is a smoker, otherwise yi = 0,

• zi = 1 if life i is female, otherwise if life i is male zi = 0,

• βx, βy, βz are the regression coefficients corresponding to the three covariates.

After estimation the following estimates were found for the unknown parameters: µ0(t) = 0.005e0.01t , βx = 0.01, βy = 0.2, βz = −0.05.

(a) Determine the (residual after entry) hazard, cumulative hazard and survival function of person A: a male smoker aged 30 at entry and person B: a female smoker aged 40 at entry.

(b) Determine the relative risk of person A relative to person B.

(c) Determine the hazard, cumulative hazard and survival function of the residual lifetime at time t = 3 of a female non-smoker aged 45 at time t = 3.

(d) In the current model the time scale is time elapsed since entry and age is a covariate. One could also think of a somewhat simpler Cox PH model where the time scale is the age of the policyholder and the only covariates are the categorical covariates yi and zi . Give a reason why the modeller has opted for the current model instead of the simplified version, i.e. why might the modeller have chosen for the time scale to be time elapsed since entry.

** Exercise 1.4

Let T be a survival time (satisfying the assumptions made in the beginning of Section 1.1 of the notes) with hazard function µ(t) and survival function S(t).

(a) Let g(t) =  h(u)du, where h is a positive, integrable function. Show that

h(u)du, where h is a positive, integrable function. Show that

(b) Assume  and compute E[T|x] for any x ≥ 0, where T|x denotes the residual survival time at time x. (Hint: use part (a).)

and compute E[T|x] for any x ≥ 0, where T|x denotes the residual survival time at time x. (Hint: use part (a).)

(c) Use part (a) to show that for any b > 0, E [T1{T ≤b}] =  S(t)dt − bS(b).

S(t)dt − bS(b).

* Exercise 1.5

Prove the identities in (1.4) of the notes.